After completing your detailed scoring for impact and financial materiality — and considering input from stakeholders — the final step is to assign an overall materiality score to each topic.

This overall score determines which topics are material and will move forward into your ESG policies, actions, targets, and reporting.

Defining What Counts as Material

Each organisation decides what score range qualifies as “material.” For example:

-

Conservative approach: Only topics scoring 4–5 are considered material

-

Broader approach: Topics scoring 3–5 are considered material

You should define this threshold internally based on your:

-

Sustainability ambitions

-

Reporting obligations

-

Stakeholder expectations

Klappir‑Strategy supports both approaches. What matters is that your organisation is clear and consistent — especially when linking material topics to the next steps in your sustainability work.

What to do in Klappir‑Strategy

-

Open each topic in the Materiality Assessment module

-

Review your detailed scoring (impact + financial) and stakeholder comments

-

Assign an overall materiality score (1–5):

| core | Description |

|---|---|

| 1 – Not applicable or minimal | No meaningful relevance |

| 2 – Low | Limited relevance; unlikely to require action |

| 3 – Moderate | Relevant; monitor or explore further |

| 4 – High (Material) | Material issue; requires action or reporting |

| 5 – Very High (Material) | Critical issue; strategic priority |

Use the Comment field to explain your rationale — especially for borderline or stakeholder-sensitive topics.

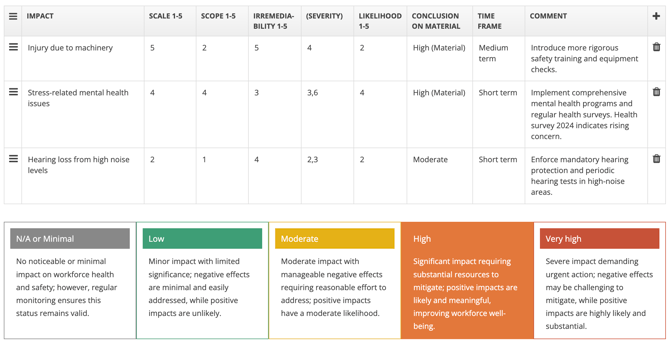

1. Determining Impact Materiality

A topic is considered material from an impact perspective when one or more of its underlying issues is likely to lead to significant actual or potential effects on people or the environment.

While High or Very High scores are strong indicators, you may also mark a topic as material based on:

-

Several Moderate impacts that collectively carry significance

-

Stakeholder concerns or sensitivity

-

Strategic or reputational priorities

Use your professional judgment, and document your reasoning in the Comment field to ensure traceability.

You can refer to the severity score (based on dimensions such as scale, scope, irremediability, and likelihood) as a supporting reference.

Example: Health and Safety Impacts

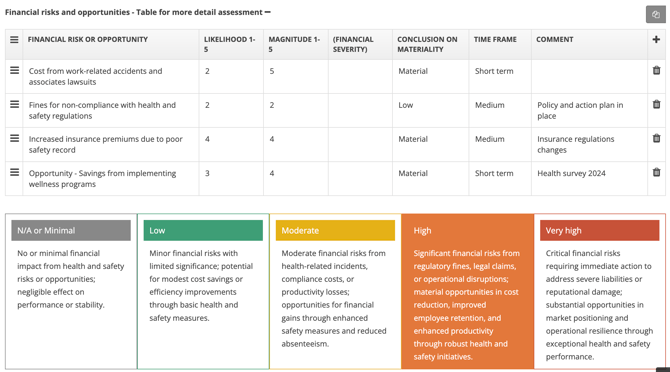

2. Determining Financial Materiality

A topic is financially material when one or more risks or opportunities under it could significantly affect the organisation’s financial performance — in the short, medium, or long term.

While High or Very High magnitude and likelihood scores are strong indicators, you may also consider:

-

Several Moderate risks or opportunities that together pose a meaningful concern

-

Strategic or business-critical themes

-

Financial or ESG expectations from key stakeholders

Again, use your professional judgment and document the rationale in the Comment field.

You may refer to the financial severity score (average of magnitude and likelihood) as a supporting reference, although this is not calculated automatically.

Tip: You can refer to the calculated Financial Severity score (average of Likelihood and Magnitude) as a supporting reference.

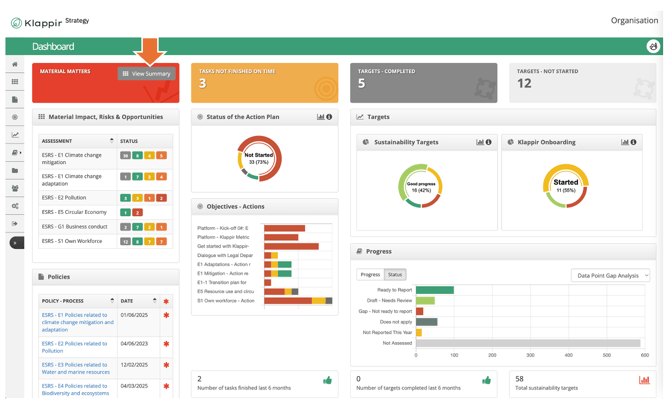

3. Dashboard and Summary View

Once topics are scored:

-

Material topics (typically scoring 4–5) appear in your Dashboard view

-

Use "View Summary" in the Materiality module to access:

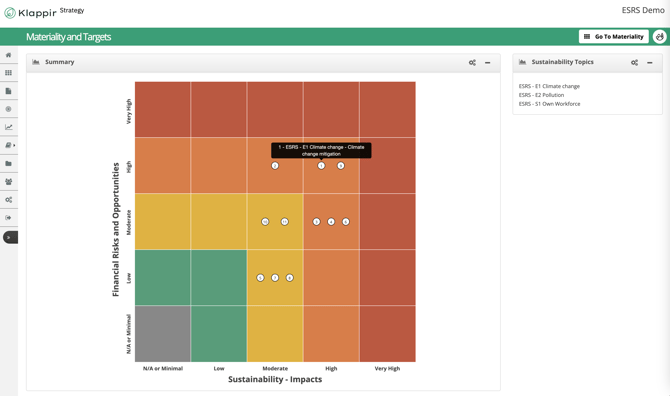

-

A heat map showing prioritised topics

-

Lists of all impacts, risks, and opportunities by topic

-

Clear visual and textual overviews of your double materiality assessment

-

You may also revisit this summary to support internal discussions, stakeholder validation, or ESG rating reviews.

View Summary Report

You can also access the materiality assessment summary by pressing on "View Summary" in the Materiality module

![]()

Standards Alignment

| Standard | Expectation |

|---|---|

| ESRS (Draft July 2025) | Requires clear identification of material topics based on impacts and/or financial relevance. Final decision lies with the undertaking. See ESRS 2 IRO‑1 and IRO‑2. |

| VSME | Topics are marked “Applicable” if relevant. Scoring is optional but using a 1–5 scale enhances consistency. Threshold for materiality is determined by the organisation. |

Go to the next chapter: